Each year, investors are led to ask themselves the question of the strategy to adopt for the period to come. However, if the annual periodicity makes it possible to take a regular update, to carry out certain arbitrations (possibly due to taxation), having a short-term approach is not necessarily the most rational approach. Indeed, a successful investment approach will take into account liquidity constraints. This will adopt a diversified approach in order to optimize the risk / return ratio and an approach integrating more or less long-term assets in order to maximize the expected return. This therefore goes beyond a purely annual and calendar view.

However, this end of the year may be an opportunity to take stock in terms of prospects after almost two years of the Covid-19 pandemic and while hopes of an exit from the health crisis appear. All the more so as despite the crisis, paradoxically, the valuation of most assets continued to rise to record all-time highs ...

The level of asset valuation: the question for 2022?

2021 ends with a second year of health crisis. The easing of constraints and the end of lockdowns - which have however resumed in certain regions - have allowed economies to pick up again. The rebound in economic activity also benefited from catch-up effects. Almost everywhere - and particularly in France where the purchasing power of the French has been able to be maintained despite everything - households have accumulated significant forced savings. This is now available to consume.

In France, the additional savings accumulated are estimated at around 200 billion euros. On the financial market side, after a low in 2020 at the height of the crisis, the stock markets hardly waited to resume their forward march. They even exceeded their historical levels. As for real estate assets, they suffered little overall, particularly housing. Indeed, the latter continues to benefit from strong demand. However, questions arise about business and office assets.

Stock markets at their highest: is it sustainable?

Globally, the American (S & P500, Nasdaq), Asian and European markets have all experienced historic highs this year. In terms of ratio, the American markets have largely returned to the valuation levels known on the eve of the 1929 crisis ... Japanese markets have reached their record level of 1990 which preceded the "crash" of its economy. For its part, the CAC40 has for the first time exceeded 7000 points. It thus broke the record known during the internet bubble in 2000 (by including dividends received by companies: the gain would have been + 92% over the period).

However, can we put the levels reached into perspective? The rise in the CAC40 since the start of 2021 is + 27% (and a rebound of almost x2 from the low point of the first confinement in 2020). And this, with for the first time the threshold reached of 7000 points. But, this could be explained in part by an equivalent increase in the profits of the companies making up the index and good prospects. Moreover, historical comparisons are sometimes difficult.

Thus, during the internet bubble and the previous record, the CAC40 index had a strong technological component with a strong presence of “goodwill” and sometimes unprofitable assets on the balance sheets. While one of the big current winners is the luxury sector which has significant margins. Moreover, from the point of view of an international investor, the value of assets in euros has depreciated by more than 8% since the start of 2021. This is due to the strong appreciation of the $ / € parity.

Across the Atlantic, the markets have been driven in particular by companies in the tech sector. Among the latter, some: Apple, Tesla, Facebook, Amazon now have a capitalization sometimes exceeding 2000 billion individually. This represents more than the total valuation of the French market ... With sometimes stratospheric levels anticipating changes. But, also expected future growth rates for companies which have seen their fundamentals driven by accelerated digitization of the economy.

Many savers, comforted by recent periods, have also become investors. Whether on the stock market (or in other assets such as Bitcoin). And this, to invest in it among other things the checks paid by the administration in the context of the health crisis. The analysis of the overseas context is however different from France. Indeed, Americans are by nature massively exposed to financial markets. And this, in particular through their funded retirement plans.

French companies have rebuilt their margins

Another point to take into account: the level of margin rates of French companies has reached an all-time high since the post-war period. However, this figure must be moderated:

An economic catch-up effect following the confinement episodes;

The positive impact of supporting activity and businesses. As well as the policy of whatever costs (reduction of charges, partial unemployment, etc.);

The threats posed by a return of inflation and an increase in costs (raw materials, energy, wages, etc.;

The significant level of margin would also correspond to an economic need to finance business models that require much more investment. And this with the resulting depreciation of assets. But also, the obligation to generate sufficient cash flow to finance these investments.

"FOMO" and "TINA" powerful vectors?

Whatever the asset classes, investors in the current context can be teased by two phenomena:

The TINA observation “There Is No Alternative” (there is no plan B ”). This approach starts from a rational observation: the risk is currently very poorly remunerated. Indeed, the rates are at their lowest (life insurance for example) for risk-free assets. In this context, this pushes a shift towards riskier and more liquid assets such as the stock markets. Indeed, in a context of a possible upturn in inflation - which is eroding the wealth of inactive investors - doing nothing does not seem an option. And this, at the risk of sometimes “overpaying” the investments;

FOMO “Fear Of Missing Out”. This amounts to confirming the fact that beyond the fundamentals, valuations are above all the result of a confrontation of supply and demand. In a bullish environment, and with 24/7 real-time access to a wealth of information and investment opportunities, investors are encouraged to "jump on the bandwagon" (the most cynical will apply the "idiot theory" (consisting in buying an asset not for its fundamentals, but because they believe that because of the momentum there will always be another investor ready to buy it back at a higher price).

Are Financial Markets Too Expensive?

By definition, stock markets obey the law of supply and demand. When liquidity is plentiful, it pushes up asset prices. In addition, low interest rates encourage investors looking for a certain return to buy riskier assets. And in particular, risky assets such as stocks. In addition, low rates are supposed to promote economic activity and consequently the performance of companies.

Investing in equities necessarily involves looking to the future, taking into account the development potential of companies. To take a cartoonish case: the automaker Tesla (whose founder Elon Musk has become the richest man in the world) has taken an innovative approach in the field of electric cars. However, its capitalization alone is already worth more than that of all the other players in the automotive industry. Some will say it is justified due to the growth of the company despite low market share, others will say it is overkill.

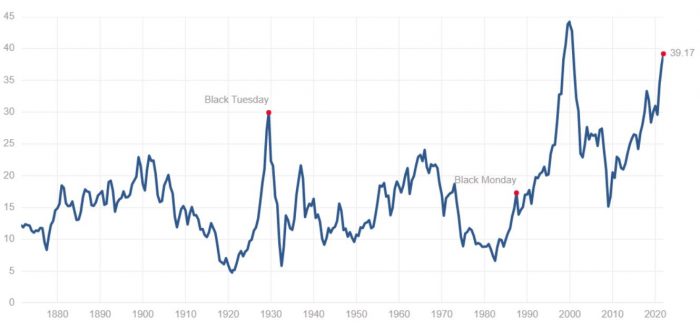

From a global point of view, the CAPE or Shiller PE index makes it possible to relate the price (or capitalization) of shares to their implicit multiple compared to the profit generated by companies. This tool is not perfect and deserves to be supplemented by other analyzes (growth, etc.). However, it makes it possible to objectify a more or less high level of the markets.

Cape Shiller pE from s & p500, to 11/30/2021

The real estate market in a still positive dynamic

The real estate activity as a whole ended the year with a bang. And this, whether in terms of the number of transactions or the level of prices per m². In general, in France, the demand for housing is still strong. A safe haven par excellence, real estate seems to have largely respected its reputation in 2021:

The prices continued to rise. And this, to a lesser extent in the capital, and more markedly in Greater Paris. But also by capillarity in the main metropolises and in rural areas (whose price index has returned to the level before the 2008 crisis). Driven by various trends (teleworking, second home, etc.) many French regions have taken advantage of this trend;

SCPIs (94% invested in commercial real estate, mainly office buildings) have regained good momentum. They kept yields above 4%. Without however returning to the 2019 records in terms of collections and yields. Certain themes such as health, education, logistics or diversified portfolios are particularly appreciated. The office is still the main classroom. And this, despite the questions about teleworking. Nonetheless, assets linked to trade, hotels, tourism and leisure have experienced more difficulties;

The tax schemes in favor of rental investment (Malraux, Pinel, Denormandie, etc.) enabling income taxes to be reduced have remained in place. The financing and mortgage conditions are still very favorable.

In addition, the covid-19 crisis was an opportunity to accelerate certain trends. Whether it is: the development of e-commerce and logistics, territorial decentralization. Or the appearance of new formats facilitated by digitization (flex-office, co-working, coliving, etc.).

The fact remains that the tendency to decorrelate household income and the value of real estate remains. Even so, historically favorable borrowing and financing conditions (rate 1.05% over 20 years and average duration of real estate loans 233 months) have generally made it possible to maintain the real estate purchasing power of the French.

Real estate loan conditions tightened in 2022

The ratio of household debt to their disposable income has doubled in 10 years. The HCSF (Haut Conseil de Sécurité Financière) has also taken up the subject. From 2022, it will impose restrictions on banks for granting real estate loans:

35% effort rate (net income on monthly debt payment) maximum;

Maximum duration of 25 years in old and 27 years in new.

While most of the investment tax systems (Pinel, Malraux, etc.) have been extended, the Climate and Resilience law will also impose new constraints on homeowners. And this, in terms of energy and environmental quality, which should be gradually implemented over the next few years.

In any case, more than ever, investing in real estate will undoubtedly mean always being more selective.

2022: year of prudence?

The observation of an "irrational exuberance" of the markets - according to the famous phrase pronounced in 1996 by Alan Greenspan, former President of the Federal Reserve of the United States - had nevertheless preceded by several years the historic peak of the stock market and the " internet bubble ”. If there is no ideal timing to invest, can 2022 be a pivotal year?

Irrational exuberance of the markets?

Many voices have started to rise in recent years to question the valuation levels reached by most assets. The economies - but above all the price of assets - have in fact been massively supported since the “Subprime” crisis by the “accommodating” policies of central banks. These policies have led to negative interest rates, fueled by massive asset buybacks from central banks. With very low risk pay, investors tended to shift towards risky assets. Until the creation of bubbles?

In any case, this is the thesis put forward for example by financiers such as Georges Ugeux in “The Descent into the Underworld of Finance” or more recently Laurent Berrebi in “Money and capital: The new heritage economy”. Highlighting the essential role played by the accommodating policies of central banks.

Leading players such as Warren Buffet have reduced their investment in 2021 (accumulating a record amount of cash of 159 billion dollars). Partly missing the increase in recent quarters but thereby showing a certain caution.

2022: the return of inflation?

Inflation is said to have reached 6.2% in the United States and 4.2% in the eurozone, a level unknown for decades. In addition, we are seeing a sharp rise in employment everywhere. As well as lower unemployment rates and upward pressure on wages.

It is difficult to say, however, whether inflation will be maintained over the long term or whether it is partly a temporary phenomenon. Indeed, supply difficulties - with some factories idling - faced with a recovery in demand is fueling price increases. The recovery has in fact led in the short term to restocking operations (sometimes leading to supply disruptions and real shortages as is currently the case in the automotive industry) as well as an inflation of logistics costs. In addition, the costs of energy and raw materials have reached all-time highs.

The GDP growth forecast in France for 2021 is over 6%. Either a rebound in activity rarely seen. However, we must put it into perspective. It is above all a return to the level of 2019 after the lows caused by the health crisis, a kind of return to normal.

Towards a rate hike?

Jérôme Powell - who is classified rather as a pragmatist - has just been reappointed by Joe Biden at the head of the FED. Regarding the ECB, its president Christine Lagarde did not specifically send a message in the direction of an upcoming rate hike. Ditto for the Bank of England. No very clear message for the time being therefore on a timetable for raising the key rates of the various central banks.

However, the latter have started to reduce their asset buyback program. However, by repurchasing assets, banks increase the demand for these assets (e.g. bonds). They therefore help to keep rates low, or even negative. Interest rate levels are the point of equilibrium between supply and demand for debt. Thus, by increasing demand, central banks push yields down.

However, if the inflation outlook is confirmed and monetary policies become less accommodating, interest rate levels will inevitably rise. This movement seems to have already started slightly.

The negative impact of a rate hike on activity and asset prices

In theory, a rate hike has two consequences:

It makes debt more expensive and the financing of new projects less easily profitable. Indeed, the cost of financing must remain lower than the expected gain from the project for the investor. (And for the banker, a higher amount of interest implies an all the more qualitative project to be eligible for financing);

It contributes to a fall in the price of assets. Indeed, with high rates, it is less easy to borrow and obtain liquidity. This further reduces the "budget" available to investors. In addition, the level of interest rates is used to calculate the price of assets: this is called "discounting". So, for example, if an asset gives me the following 5-year flow sequence: $ 5 / year received for 4 years and $ 105 ($ 100 + $ 5) in the last year, I'd be willing to pay it today. hui $ 100 if I aim for a 5% return. But, if I aim for a 10% return on the same investment, I'll reduce the price I'm willing to pay to $ 81. However, performance requirements are linked to individual objectives. Corn,

What health situation in 2022?

2021 will have seen certain political risks crystallize or unwind (election of Biden in the United States for example). But also a turning point in the situation of the health crisis, which we hope will be decisive, with the appearance of vaccines to fight against the Covid-19 pandemic.

However, the risk linked to the epidemic is still not completely ruled out as evidenced by the return of confinements in Europe or the appearance of new variants such as Omicron in particular. Between supply shortages and possible reconfigurations, it is difficult to project a real pace of economic recovery.

The challenges of 2022?

Economically, will 2022 be the year of headwinds? As the economic recovery appears to be taking hold, new challenges could undermine the dynamics of the economic recovery:

Gradual end of massive state budget support to economies?

Unknown whether households will build up and maintain precautionary savings or increase their consumption;

Difficulties of supplies and risk of shortages or on the other hand end of the "catch-up" effect;

Possible start of a cycle of interest rate hikes and end of “quantitative easing” by central banks;

Possible rebound in the health crisis and the Covid-19 pandemic.

Allowances 2022 what to do?

In its November 2021 press release, the ECB's Financial Stability Committee pinpointed the risk of a correction in certain markets. And this, by taking up the term "exuberance". For its part, the Morgan Stanley bank ,

in a recent economic update , questioned the impact of a reduction in public intervention. In particular with the end of "whatever the cost" and the support of central banks. Using the colorful expression “training wheels are coming off” the Bank has synthetically illustrated the impact on the economy. But also the different markets that such a movement would represent. Thus calling for caution in the medium term.

Investing in 2022: having and taking your time?

Some banks such as Amundi wondered about a possible return of stagflation (a return of inflation, but without growth).

In times of uncertainty, there is no need to rush. In addition, a rise in rates could impact asset prices. All the more so if they have a long duration (that is to say that their price is strongly impacted by a variation in rates).

Should we opt for shorter investment periods, or long-term ones? Still, one should probably not be overly exposed or have liquidity constraints (risk having to resell one's assets quickly) given the possible fluctuations in asset prices. Investing more regularly can also be a way to reduce uncertainty. In other words, "have the time and take your time".

Leverage: the best enemy?

With historically low rate levels, it's tempting to take advantage of leverage. In particular, by financing part of its investment through debt at an almost free cost. In the long run, this can undoubtedly be a winning bet. Especially since in residential real estate, for example, the amount of loans is calibrated on the level of income and not linked to the valuation of assets.

In the current context, an uncontrolled leverage effect (and backed by the value of assets or a forecast return) can prove to be very risky in the event of turbulence and strong valuations. Nothing worse than being forced to sell an asset at the worst time to meet your debts. Keeping a sufficient safety margin (haircut) between the value of the assets financed and the debt is undoubtedly preferable. Being cautious about projected income and debt service, avoiding illiquid assets is arguably more necessary than ever. This is in order to take advantage of favorable interest rate conditions without overexposing yourself to uncertainties.

Seeking returns to invest your money

In recent years, we have seen the era of zero returns on risk-free assets. However, this had the consequence of favoring another type of return: that resulting from the capital gains generated on resale by the rise in the price of assets (real estate, shares, bitcoin, etc.). Valuations themselves were pushed up by the influx of liquidity from central banks. As well as the favorable credit conditions, which encouraged investors to invest in assets whose price was promised to increase to the detriment of the intrinsic return (coupon, rent, dividend, etc.).

The new paradigm can, however, encourage people to detach themselves from the search for surplus value at any cost:

Favor "value" management by favoring assets that offer a certain recurrence and a rather high return;

Open up to alternative assets: real estate crowdfunding, for example, offers returns of 8% to 10% with rather short maturities. But also programmed liquidity, and strong diversification possibilities. Of course, it remains to assess the level of risk by setting up a necessary level of security (surety, mortgages, etc.). Or by diversifying and avoiding strong leverage effects as well as obvious illiquidity risks.

Faq:

Where to invest in real estate in France? In which city should you invest in real estate in 2022?

In the case of a main residence, the location of the purchase will by nature be implicitly fixed (the decision to buy or rent remains to be taken, etc.). In addition, with the development of teleworking and the attractiveness of second homes, secondary cities and coastal areas have experienced a particularly marked increase. Greater Paris has also benefited from the trend, as has intramural Paris to a lesser extent. The context was that of a continuation of a general increase in house prices. The price index for rural areas even returned to its 2008 level.

For a rental investment, beyond the attractiveness of the city (university city, economic hub, transport, living environment, etc.), the Real Estate Tension Index (ITI) can help measure land pressure and balance between supply and demand. In some areas under stress, there are still tax measures (Pinel, Malraux, Denormandie, etc.) which allow significant tax savings to be made. And this, through the purchase of a new property (or old property to renovate) with a rental commitment for a minimum period (generally 9 years). To be eligible, in addition to respecting the rental commitment, certain criteria may have to be met. Whether: the location, type of work, amount invested,

Depending on the city, the rental of furnished accommodation (which corresponds to shorter leases and a specific offer) may be indicated. On the other hand, it can make it possible to obtain a higher yield. But, above all, to benefit from the LMP and LMNP tax regimes which make it possible to greatly reduce the tax on property income.

French: a net salary between 2,000 to 3,000 euros how many square meters in 2022?

According to INSEE , a full-time employee in the private sector earns on average 2,424 euros per month. And this, of course, with disparities (half of the employees receiving less than 1,940 euros net per month).

Furthermore, according to the Notaries' index , the median price in France would be 2,280 euros / m². Against nearly 10,880 euros / m² in Paris.

Based on the new rules soon in force (35% maximum effort rate), the maximum monthly annuity will be 848 euros. This represents a maximum loan of 220,000 euros (over 25 years, at the rate of 1.14% / year excluding borrower insurance). And this, excluding notary fees, and without personal contribution. It would thus be theoretically possible to finance 97 m² on average in France and 20.5 m² in Paris.

Which profitable investment in 2022: the year of trading or of the long term?

In sometimes uncertain times, aiming for liquid assets and trying to optimize (or even generate a positive performance in a bear market) by playing on volatility can be tempting. However, statistics seem to show that it is often illusory to want to beat the market by adopting the ideal timing. Indeed, the risk of intervening often at the wrong time is high. Even experts using artificial intelligence algorithms cannot necessarily predict market fluctuations. This is also often a criticism addressed to expert professional asset managers. In the long term, these do not necessarily manage to beat the performance of passive management (replicating indices) via an ETF for example. Even more so,

While there is no ideal solution, taking a long-term approach is often good advice. This does not achieve maximum yield, but is still a good approach. In the absence of ideal timing, the strongest variations in the market will be absorbed. A prerequisite - or a golden rule -: have a sufficient horizon in terms of liquidity. In addition, rental investment sometimes makes it possible to self-finance the investment in debt. However, this should be more difficult in 2022 with the constraints imposed on banks.

Looking for the right profitable investment in 2022: what to invest in on the stock market? The remaining shares little expensive ?

In absolute and relative terms, the level of stock markets around the world appears to be high. Nevertheless, it is possible to adopt differentiated investment themes. For example, stocks linked to new technologies have benefited (probably in part due to) from their strong growth. As well as the increasing digitization of the economy. Their valuation is however the most likely to be impacted by a rise in rates. Conversely in a context of economic recovery, it may be advisable to buy cyclical stocks, for example, in certain sectors (capital goods, luxury consumer products) because they present a recurring business and offer a higher yield. raised. The decision must, however, be assessed on a case-by-case basis and the dispersion and performance gaps are significant.

If one wants to avoid being too selective or biased, ETFs can be a solution. Like funds, they are investment vehicles, but at little cost. They allow direct and synthetic investment in baskets of shares (or assets). Or on indices located in different geographic areas around the world.

Investing in “private equity” in 2022

"Private equity" allows relatively wealthy investors to invest directly via funds in small companies (small-caps), SMEs or ETI in the hope that they will develop. An investment reserved for investors likely to invest large amounts, private equity makes it possible to invest in unlisted companies. Private equity makes it possible to target companies looking for funds to develop or to support business buyers. This type of investment nevertheless involves a long time horizon (10 years or more). Moreover, it is inherently risky. However, it can be integrated within the framework of dynamic asset management. Indeed, depending on the stage of development of the companies, it is difficult to always make the right choices in terms of investment. The risk of capital losses remains commensurate with the expected return. Investing in the capital of unlisted SMEs also has tax advantages for investors.

What echoes for life insurance in 2022?

The yields of life insurance contracts (as well as in general of guaranteed savings accounts) - an essential investment for wealth management advisers - have fallen sharply in recent years. This is because of the drop in rates. It has even become difficult for life insurers to guarantee a positive return in a context of negative rates. Insurers have also introduced constraints in terms of investment on their "euro" contract. They now often require a quota invested in more risky media: Unit of Accounts (or UC), invested in various underlying assets (real estate, SCPI, stock exchange, funds, etc.). However, these “UC” contracts are not guaranteed (as could be a euro contract, or even a livret A).

Investing in cryptocurrencies in 2022

In recent years, the general public has discovered cryptocurrencies, a phenomenon that divides experts. Deemed by some to be an investment with high potential, intended to replace assets such as gold, cryptocurrencies such as Bitcoin have had a course that is admittedly chaotic, but almost flawless for most investors. Still close to their historic highs, cryptocurrencies (and their derivatives such as NFTs) remain highly speculative and volatile assets. It remains difficult to understand their intrinsic value. A sign of a certain institutionalization, the first cryptocurrency ETFs were recently launched in the United States.

Investing in 2022: focus on real estate crowdfunding

In the current period, with the choice between a long-term approach and a need to temporize, “ crowdfunding ” offers many advantages. Within crowdfunding, the segment of “real estate crowdfunding” makes it possible to invest indirectly in the real estate theme. And this, by financing via bonds of professional real estate actors (developers, property dealers, real estate):

In a world where the search for yield has become complicated, crowdlending offers average gross returns of 6% to 10% / year;

It allows to focus on relatively short maturities: 12-36 months in bonds redeemable or ultimately . This allows you to position yourself with a high return without having to "bet" on the long term;

Real estate crowdlending allows the establishment of real securities (mortgages, guarantees, etc.). But also to relatively secure the investment by respecting certain maximum ratios in terms of LTV (Loan to Value, that is to say borrowing in relation to the value of the financed asset);

The selection is direct for the investor. However, it remains supported by approved professionals who offer the projects on their platform;

Diversification in terms of amounts, maturity, projects and issuer is very easy (minimum amount of 1,000 euros per project);

Investments are eligible for certain tax measures such as the PEA-PME and in terms of income taxes imposed at the 30% flat-tax;

The costs of the transaction are borne by the issuers and have no impact on the investor's net return.